Key Takeaways

- Maxing out your 401k every year doesn’t mean you’re set for retirement

- You’ve been running in growth and accumulation mode for the past 30 years. Can you suddenly downshift without grinding the gears?

- Could you and your spouse sit down together for 90 minutes and have a focused conversation about what you really want out of life?

- In my opinion, do-it-yourselfers tend to miss opportunities, leave gaps in estate plans and have too much wealth tied up in their employer stock

As a successful professional with a strong analytical mind, you have the intelligence to figure out the many facets of retirement planning. But, do you really have the time or desire to do it yourself? Even if you have the time, can you honestly remain objective and keep your emotions in check when things get tense in the stock market or real estate market? How about when dealing with sensitive family estate planning issues or tax complications or charitable giving plans? Do you enjoy researching these issues or would rather spend your time doing things you love?

That’s a question that you and your spouse need to be brutally honest about answering. You may have been high school valedictorian and top of your engineering class, but there’s no way to test your “fight or flight” impulses when a tough money matter or life transition comes up.

If you’re young, in good health and have strong relationships with your extended family, then you can be a do-it-yourselfer (DIY) for a while. But, below are actual comments from successful people who’ve come to see me over the past 12 months. Eventually you’ll get to the point that you’ve accumulated a fair amount of wealth, just when life starts throwing you more curve balls. They…..

- Wished they had sold more shares of a large stock position when it reached its high three years ago.

- Wished they had waited longer to start receiving Social Security.

- Wished they had recognized how poorly their 401(k) has been performing over the last 10 years.

- Wished their spouse was contributing to a retirement account.

- Wished they took action long ago to start looking at their financial health.

- Wished they knew “someone like me” 30 years ago.

- Wished their parents had been more organized when they passed away.

Chances are you’ve maxed out our 401(k) every year. Congrats. It’s tempting to think you’re right on track for retirement. But, suppose you had a serious tax issue or an unexpected setback in your career, your family or your health? Suppose those setbacks hit you just when the markets are nosediving and the media’s urging you to hit the panic button every day? Do you have the discipline, training, expert contacts and experience to stay the course when your body’s natural fight or flight response kicks in?

“We cannot solve our problems with the same thinking we used when we created them.” – Albert Einstein

Succumbing to your emotions (see below) is not a personal weakness by the way; it’s part of our human DNA. That’s why so many people find it helpful to have a coach or accountability partner to guide them through challenging times.

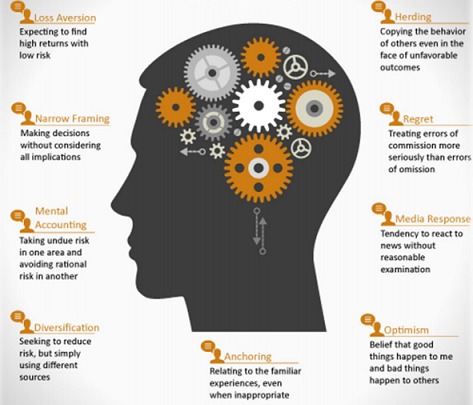

COMMON INVESTOR BAD BEHAVIORS

DALBAR, a leading financial market research firm, identified nine bad behaviors that cause individual investors to lag both equity and fixed income markets by about 3.7 percent per year (i.e. 44% compounded over 10 years!). Here’s the worst part, this underperformance occurs even though individual investors correctly guess the market’s monthly direction about 75 percent of the time!

Source: “Quantitative Analysis of Investor Behavior, 2016,” DALBAR, Inc. www.dalbar.com

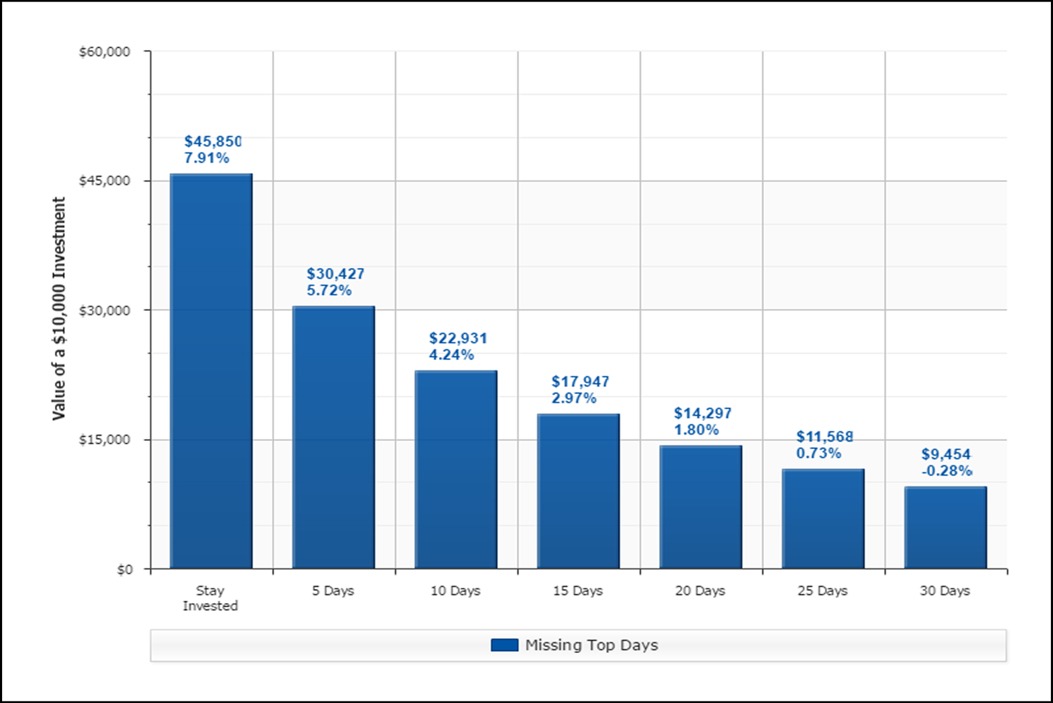

Many of these bad behaviors cause do-it-yourselfers (DIY’s) to get in and out of the markets at just the wrong time. As the chart below shows, missing out on just the 10 best days the market’s had over the past two decades would have cost you $22,919 over the 20-year period, based on a $10,000 initial investment. That’s right, you could be almost $23,000 behind someone who invested the same $10,000 when you did and never made a move.

Source: ChartSource®, DST Systems, Inc. For the period from October 1, 1996, through September 30, 2016.

3 biggest challenges for DIY’s: It’s about more than just investments

I’ve worked with many successful people who manage extremely large projects and teams. They deal with mind-numbing complexity and constantly shifting deadlines. But, when it comes to managing one’s own retirement, there are three common mistakes DIY’s tend to make:

1. BEING FINANCIALLY SCATTERED

When successful professionals reach their 50s and 60s, they tend to have multiple accounts in many different places—especially if they’ve been a DIY. This makes it hard to see the progress (or lack thereof) that they’re making toward goals such as retirement, buying a vacation home, helping grandkids pay for school, etc. Being disorganized makes it hard to have a unified investment strategy and will complicate things tremendously for your heirs when you die. Don’t be a crop duster when it comes to your financial statements and accounts.

One of the first things our firm does for new clients is build a Net Worth Statement, which gives clients a clear picture of all their assets by type (cash vs. not-cash and retirement vs. not retirement) minus all of their liabilities. In other words, what you own vs. what you owe.

For estate planning purposes we need to know the ownership status of a client’s assets (Individual/joint/trust?) and confirm all their beneficiaries. Knowing the cost basis of non-retirement assets for non-retirement assets that may need to be sold some day for tax purposes is also very important. We also build a Cash Flow Statement since most people don’t know exactly where all their money is going. How much of your income is being saved for retirement? How much goes to taxes? Where is all the rest going? Is enough being saved? If so, is it in the right type of account for a specific goal?

2. MISSING OPPORTUNITIES

You can’t go back in time to correct a mistake or do something you wish you had done and didn’t. Suppose you weren’t funding your retirement account sufficiently? Chances are you could have contributed more, but didn’t know exactly how much more you could have contributed. Had you done so at the time, you’d have been able to retire today.

Suppose you had started a health savings account (HSA) when your company first offered it? How much easier would it be to handle those out-of-pocket medical bills? You might have a lot more than you think in low-interest cash accounts. Chances are it’s more than you need for day to day expenses and your rainy day fund. Hypothetically speaking, had you invested that surplus cash reserve more aggressively 10 years ago, using historical returns of 8.7% from a 60% stocks/40% bonds portfolio, it would have more than doubled by now. (https://personal.vanguard.com/us/insights/saving-investing/model-portfolio-allocations)

Here’s another missed opportunity: By the time clients come to see us, it finally dawns on them that they should have been investing in a Roth 401(k) rather than a traditional 401(k)? They wonder if last year was the best time for a Roth Conversion. They wonder if they should have paid their property taxes in advance last year since the deductibility of property taxes, state and local income tax are now limited to $10,000 those taxes will no longer be deductible under the new tax reform rules. They wonder if they should have reduced their tax withholding from their paycheck so they wouldn’t have to wait until April of the following year–every year–to get their tax refund and allowed that money to be put to work for them.

3. TAKING TOO MUCH RISK

Early in our process, we compile a new client’s retirement accounts, pension statements, Social Security statements, and (almost-paid off) mortgage statements. It’s often a lot of legwork. Then we compare what we’ve learned about their financial picture to what we learned about their true standard of living. More often than not, it turns out they can afford to retire immediately. They don’t need to be invested so aggressively in stocks and risk a big hit to their portfolio. “Congratulations,” I tell them. “You’ve already won the race. Why not do the things you always dreamed of doing right now?”

I meet many near-retirees who have more money than they ever imagined. That’s the good part. But it also means they have more to lose than ever before. Near-retirees have a lot at stake at this point of their lives. The right advisor will answer these and other questions for you and more than pay for him- or herself. Suppose you tested yourself on your knowledge of these issues above? If you didn’t give yourself an A or a B+, you might want to discontinue your career as a DIY, before it’s too late.

As the old saying goes, “We don’t call the plumber until the pipes break.”

Many successful people don’t think they need a financial advisor or wealth manager if they’re not in pre-retirement mode. Others only think about working with an advisor if they’re facing a serious financial issue or have suddenly come into a financial windfall. By the time they do, it’s often too late.

“I’m not poor now,” you may be telling yourself. “I’ve been doing it myself for my entire adult life and it seems to be working out just fine.” I get it. But, it reminds me of the old joke about the window washer who fell off the 50th floor of a high rise. When he passed the 25th floor, an office worker leaned out the window and asked him “how’s it going?” The window washer’s response: “So far, so good.” Don’t be that guy.

The Vanguard Advisor’s Alpha concept outlines how advisors can add value, or alpha, by providing relationship-oriented services—such as cogent wealth management via financial planning, behavioral coaching, and guidance—as a primary objective of the value proposition. https://www.vanguard.com/advisorvalue

CONCLUSION

You’re a brilliant engineer and have an important role at your company. That’s why you’re so well compensated. But, after you do your job, the production engineer and reservoir engineer typically take over. Each has a very specific role and they’re very good at what they do. How well would the project go if you tried to be the production engineer and the reservoir engineer on top of your normal responsibilities? You might figure it out eventually, but could the company afford to take that risk when so much is at stake? Same goes for your retirement. Focus on what you do best, and let the experts do what they do best. Sure you can do it yourself, but more often than not, you’ll get what you paid for.

In my next article we’ll explain how to find the right advisor whose style and values are in sync with yours.