Key Takeaways

- Investing (and wealth preservation) shouldn’t be hard.

- You don’t need to be a financial genius, you just need to be patient.

- Don’t let your emotions derail a sound financial plan.

- Wealth Preservation is one of the five major concerns of my clients; the other four are Wealth Enhancement, Wealth Transfer, Wealth Protection and Charitable Giving.

Same goes for investing and wealth accumulation. Patience, nurturing, delayed gratification and adjusting to changing conditions are all part of the process. When many people think of investing, they ask themselves: “How am I going to make more money?” But for many successful professionals, it’s not about making more money per se; it’s about preserving the wealth you’ve worked so hard to accumulate. That’s especially important for those of you in the later stages of your career.

The families my team serves have already accumulated their wealth. They want to keep it, enjoy it and eventually pass it on to their heirs and favorite causes or organizations. Their primary goal is to out-pace inflation and to mitigate risk. Like a mighty Redwood, they don’t need to keep growing by leaps and bounds, they just need to maintain a healthy base and make sure nothing eats away at their roots, bark and leaves.

INVESTING DOESN’T HAVE TO BE HARD

Once you’ve done the legwork of planting the tree properly, it shouldn’t be a time-consuming, laborious process to raise it to maturity. In the same way, investing shouldn’t be an all-consuming process that requires constant upkeep. Sure, the market can be stormy and unpredictable at times, but over the long run, the market corrects itself on its own and fosters sustained and steady growth.

Did you know you could double your money every 10 years by doing very little? Sounds too good to be true, right? Well, that’s what happens if you earn just 7.2 percent per year on your money and you don’t keep taking it in and out of the market. That’s the power of compounding, one of the most important principles of finance. Note: Since 1926, a moderate 60/40 stock-to- bond allocation’s historical rate of return has actually been 8.7 percent a year—even better than 7.2 percent.

So, a wealth advisor’s role is not to be your financial genius who whispers hot stock tips into your ear. Your advisor’s responsibility is to coach you, help you keep your emotions in check during stressful times and to prevent you from straying too far from your financial plan. Most good advisors know that the basic principles of finance (see below) can be very helpful for sticking to your big picture financial plan and for preventing your hard-earned wealth from eroding.

‘BASIC FINANCIAL PRINCIPLES’ ARE YOUR FRIEND

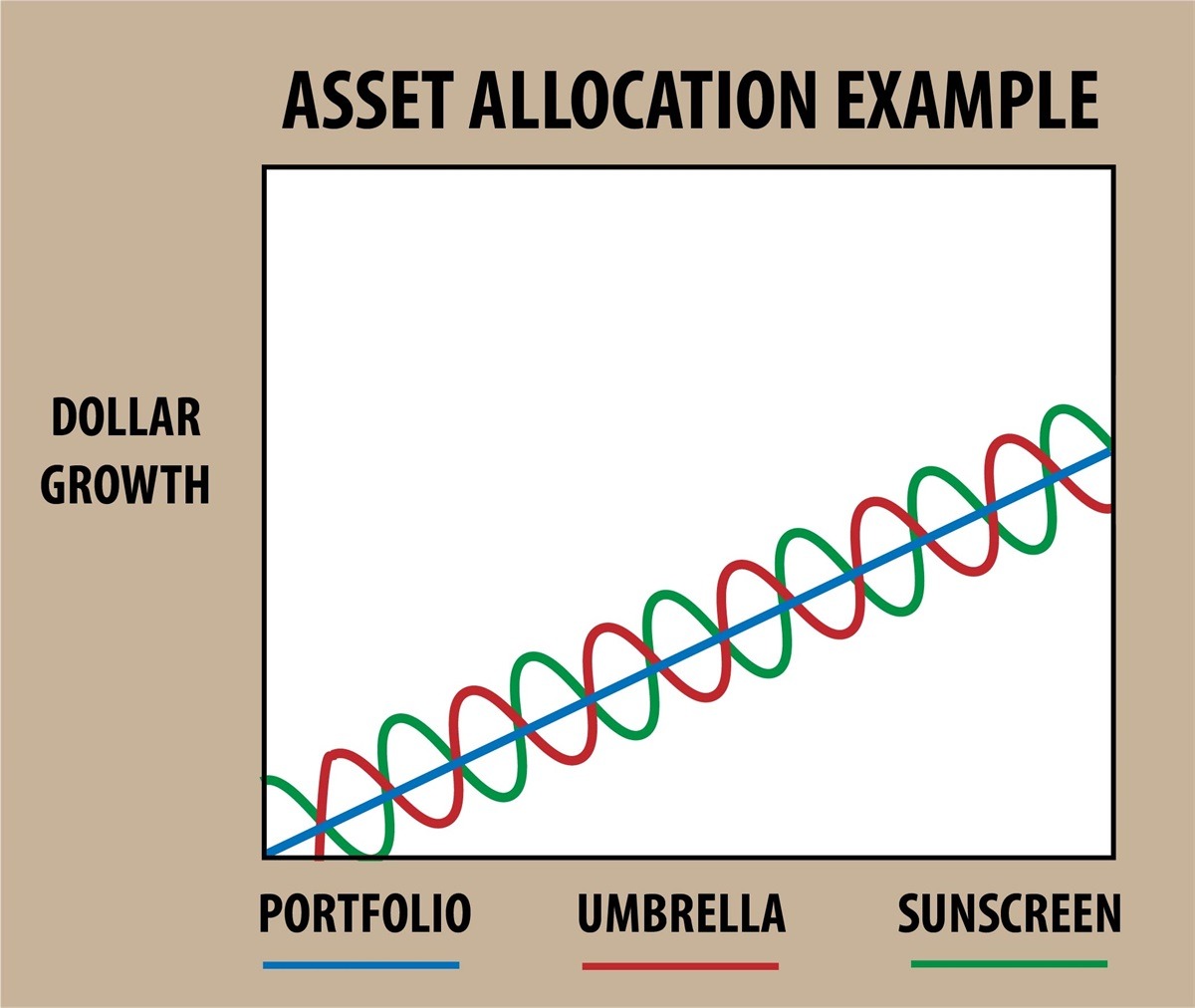

Take “asset correlation.” That’s a measure of how your various investments move in relation to one another. When assets move in the same direction at the same time, they are considered to be highly correlated. High correlation is actually a bad thing in investing because when markets go against one asset, they drag the correlated cousins down with it. However, when one asset moves up during certain times while another goes down, the two assets are considered to be negatively correlated. Negative correlation is a good thing in investing, because if one asset (or asset class) is underperforming during certain times, the other asset (or asset class) in your portfolio will step up to pick up the slack. Therefore, a basket of risky (volatile) stocks can be put together in strategic ways so that the portfolio as a whole is less risky than the individual stocks within it. This approach creates steadier growth with less risk and volatility. This is the real foundation of asset allocation and diversification. Here’s a basic example of how asset correlation works:

Sunscreen vs. rain umbrellas

Let’s say there are two companies you are considering: one that sells sunscreen and one that sells rain umbrellas. If your portfolio consists only of the company that makes sunscreen, it will have strong performance in the summer (say +50%), but poor performance in the winter (say, minus 25%). The reverse happens in the winter if your portfolio is entirely invested in the umbrella company (say, up 50% in the winter, down 25% in the summer). If you owned just one of those stocks instead of both, you could expect an average annual return of 12.5 percent long-term–but it would be a very wild ride with lots of peaks and valleys. However, if you owned equal amounts of both the umbrellas company and the sunscreen company, you could expect a constant 12.5 percent return because the two stocks are negatively correlated exactly. Why is that better than the one-stock approach? Because the two (negatively correlated) stocks would give you the same 12.5 percent return with a lot less stress and volatility.

ARE YOU SUFFICIENTLY DIVERSIFIED?

By the way, lack of diversification (sometimes called “concentration risk”) doesn’t just mean you own too few number of stocks. Even if you owned stock in 20 different companies, but they were all in the same industry, inside the same economy, you wouldn’t truly be diversified. Although you wouldn’t lose it all if one company went bankrupt, these stocks would likely be highly correlated and behave very similarly. This is why a truly diversified investment portfolio and asset allocation will own not just different types of investments, but also different sizes, industries, growth goals and geographical locations.

Like pruning a tree as needed, rebalancing is an important function of keeping your portfolio properly allocated over time as some “branches” will grow faster than others. To do this correctly you only need a little bit of trimming, not a complete tear down. The goal is to maintain your originally designed allocation and risk tolerance as time marches on and as conditions change.

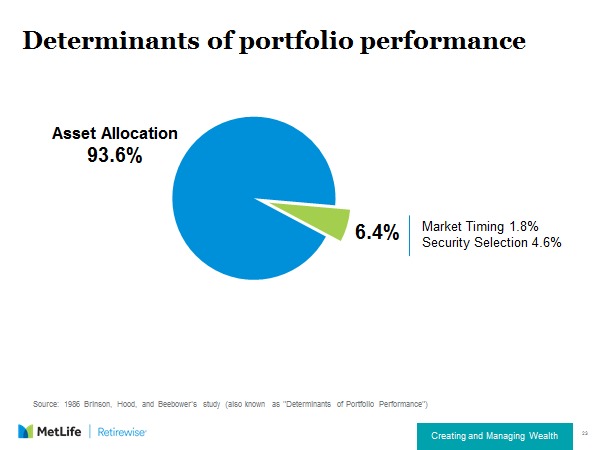

Research shows that only 6 percent of a portfolio’s long-term success can be attributed to market timing and individual stock selection (see image above). The vast majority of performance (94%) can be attributed to smart asset allocation*, which is essentially letting natural market forces do the work for you. Asset allocation is a lot less work and stress than trying to time the market and pick hot stocks (see below).

*Asset allocation does not guarantee a profit or protect against loss in declining markets. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio or that diversification among asset classes will reduce risk.

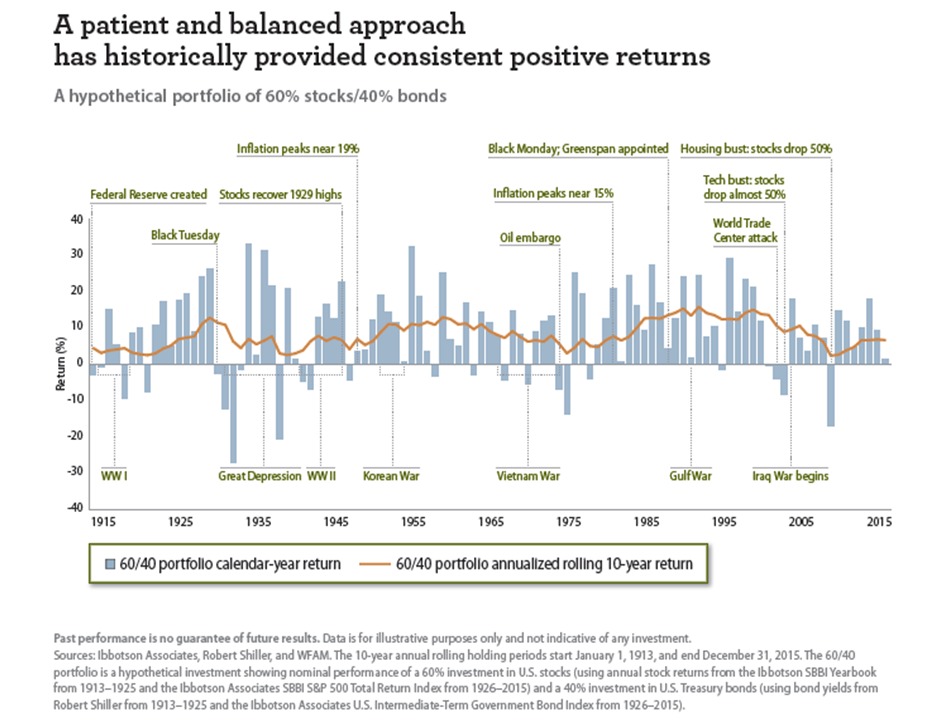

Still not convinced about the value of a well-diversified portfolio? Take any rolling 10-year period over the past century. If you had a well-diversified portfolio, you won’t find a single interval in which the market went down (see chart below). That includes 10-year periods that endured The Great Depression, the S&L Crisis and the Sub-Prime Mortgage Crisis.

REAL-WORLD EXAMPLES: BEING OVERLY CAUTIOUS IS JUST AS DANGEROUS AS BEING TOO AGGRESSIVE

Ignoring the headlines is hard to do these days. We’re inundated with stories about the next hot company, the next hot sector or even the next hot asset class (think Bitcoin). At the same time, pundits and commentators predict doom and gloom every time there’s a 100- point drop in the Dow Jones Industrial Average (not even a 1% drop today). Everyone reacts differently to bad news when it comes to their money, but emotion is a powerful driver of irrational decisions. This doesn’t make someone unintelligent, just human, as we all cannot help but be compelled by our primal emotions. The following case study involves hypothetical couples, with various realistic experiences and is provided for illustrative purposes only. Due to the complexity of each scenario, we have combined them and are providing the solutions that were most applicable to their situation. The strategies provided may not be specific or applicable to your situation.

This case study does not constitute a recommendation as to the suitability of any investment for any person or persons having circumstances similar to those portrayed. Please consult a financial advisor regarding your individual situation. Past performance does not guarantee future results*.

MARY AND TED: TWO CAUTIONARY TALES

Mary is a well-educated engineer I know who sold all her investments during the summer doldrums of 2016. Why? Because she believed the markets were stagnating and that the long-running bull market was finally out of steam. With the forthcoming 2016 Presidential election and how this could impact her plans to retire in 2 years, she sold all her stocks in late 2016. Mary put all the proceeds into cash. It was only temporary as she planned to reinvest the idle funds as soon as the stock market tanked and began its next recovery. Just one problem with Mary’s plan; the market never tanked in late 2016 or throughout 2017. She missed out on the entire synchronized global market rally—which drove most U.S. stock indices up by at least 20 percent.

Mary’s lesson: After the summer of 2016, Mary was never quite sure when to get back in to the market. Fear led to bad market timing which ultimately led to missed opportunities for growth. Ralph is very different from Mary. He’s a calculated risk-taker. As an engineer, Ralph uses mathematical formulas all day long to solve very complex problems. Ralph ran some numbers one weekend and figured the takeover stocks he was eying would get a nice bump from the acquires who would pay a premium to take control of them. What Ralph didn’t realize was that once potential acquisitions are announced to the public, the implied bump in the company’s stock price is instantaneously baked into the price. This is because there are so many investors, with lots of resources, and so much to gain by being the first, the stock price adjusts the changing demand in the blink of an eye. That’s ‘The Efficient Market Theory’ at work.

Even worse, to make up for his losses from speculating in takeover stocks, Ralph started trading every week or two in hopes of timing the market—i.e. buying a stock before its price spikes up and then selling it right after the spike occurs. Ralph occasionally got lucky with this strategy, but more often than not, he just seemed to be unlucky and racked up lots of transaction costs along the way. This is because the stock market does a “Random Walk” as described by Princeton economist Burton Malkiel in his 1973 book. Although the market has historically gone up most of the time, it does not have any discernible pattern. You want to invest for the long term growth, not gamble in the short term luck.

Ralph’s lesson: He learned the hard way not to go against two longstanding principles of empirical financial research. (1) Efficient Market Theory states that the stock market is so broad and moves so fast that prices instantaneously account for all known information in the market. (2) The Random Walk Theory states that there are simply too many variables in the market that can impact stock prices. This dynamic makes it virtually impossible to know when to buy low and sell high.

CONCLUSION

As with planting a tree, being patient, pruning occasionally and staying calm when storm clouds approach is the best path to healthy growth and enjoying the shade it provides. This will not be achieved by getting impatient, staring at the tree growing, over watering or even ripping the tree out to try to find more fertile soil. A skilled financial advisor can do the worrying for you and coach you through the ups and downs of market cycles and changing life circumstances.

Commonwealth Financial Network® or Screaming Eagle Wealth Management do not provide tax or legal advice. Please consult a tax or legal professional for advice regarding your specific situation. Erik P. Dullenkopf, CFP® (CA Insurance license #0F97513) is a Registered Representative and Investment Adviser Representative with/and offers securities and advisory services through Commonwealth Financial Network®, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through CES Insurance Agency or Screaming Eagle Wealth Management. The preceding case study is provided for illustrative purposes only and may not be representative of the experience of other clients. Every situation is different and actual performance and results will vary. This case study does not constitute a recommendation as to the suitability of any investment for any person or persons having circumstances similar to those portrayed. Please consult a financial advisor regarding your individual situation. Past performance does not guarantee future results.