Key Takeaways

- Make sure your health insurance coverage is seamless and that you have a policy with benefits and a premium that’s ideal for you.

- If you still need life insurance, your best option depends heavily on your medical history.

- Don’t let your retirement success depend solely on the stock price of your employer

- Work with a professional to determine whether utilizing Net Unrealized Appreciation is right for you.

In Part 1 of this article series, we discussed the importance of getting your financial house in order before unfortunate surprises hit. This includes knowing what to look for in a severance package and building accessible savings outside of your retirement account if you are impacted by a layoff or other life emergency. In Part 2 we discussed six key financial considerations when you are impacted by a workforce reduction. Here we will discuss ways to maintain your health and life insurance coverage if you lose your job. We will also discuss ways to get the most out of your accumulated employer stock.

CONTINUE HEALTH INSURANCE

If you lose your job in the later stages of your career, you will have some important healthcare decisions to make. That’s because Medicare does not kick in until age 65. If you are still working at age 65 or older, then you don’t have to participate in Medicare and you can continue to use your group plan. But if you are laid off BEFORE age 65—or if you decide to retire before 65—then you may be asking yourself: “How am I going to fill in that gap?”

Option 1: Take advantage of your former employer’s retiree medical plan if it has one. A retiree medical plan is a generous benefit. Just be aware that certain eligibility requirements come into play. For instance, some companies use a “points” system to determine whether or not you qualify. You may need a minimum of 80 points to qualify (i.e. age 60 + 20 years of service or age 57 + 23 years of service). If you do qualify, then for the next five years, you can stay on your former employer’s health plan and it will be very inexpensive (typically around $250 per month for a married couple). Again, many companies do not offer a retiree medical plan, so it’s likely you’ll have to pursue other options.

Option 2: Check to see if you can join your spouse’s health plan. If your spouse works and is eligible for a group health plan, then a layoff is usually considered a “qualifying event.” This will allow you and your spouse to jump onto that plan. In most cases, joining your spouse’s plan is less expensive than going out on the open exchange or maintaining a separate health plan for yourself.

Option 3: If your spouse does not work, or works for a small company that has no employee health plan, then you must resort to either the COBRA plan or Covered California (California’s version of the Affordable Healthcare Act).

a) The COBRA plan (Consolidated Omnibus Budget Reconciliation Act), allows you to remain on your former employer’s plan for up to 18 months after terminating employment, but you will have to pay the premiums in full yourself. Your employer won’t be subsidizing them.

b) Covered California The best part about Covered California is that you will be accepted even if you have pre-existing medical conditions. This can be invaluable to someone lacking access to the options listed previously. You may or may not be eligible for government subsidies here, depending on your household income. In order to sign up for a Covered California plan, you need to have a qualifying event (such as a layoff, or discontinuance of COBRA) or wait until the next open enrollment period to begin. Also, if your employer offers to pay for the COBRA during the early stages of your layoff period—I have seen coverage ranging from six months to the duration of the worker’s severance payout—it is NOT considered a qualifying event when your former employer stops paying. This means you will have to wait for open enrollment if you want to switch plans.

NOTE: Health coverage is extremely complicated these days. There are independent health care consultants who can help you evaluate various options and to determine whether it’s better to stay on COBRA or go out on the open exchange. Your income, health and age all come into play. If you don’t know such a specialist, we will be happy to refer you.

LIFE INSURANCE

Most workers can obtain basic life insurance and voluntary supplemental life insurance through their employer. It’s an invaluable way to protect your family’s economic well-being if you die during the early or mid-stages of your career. However, if you leave your employer—or are forced to leave—there are several ways to maintain life insurance. Just make sure you really need it before spending the time, or money, to obtain a new policy.

In most cases, you’ll want life insurance if you are 40 years old and have young children and a mortgage. Life insurance is especially important if you don’t have significant savings built up, which is often the case for younger workers. But, if you are over 60 and you and your spouse have sufficient assets to maintain your standard of living for another 30 years, then you don’t necessarily need life insurance for income replacement. Older couples often decide to continue their life insurance coverage because they want to provide immediate liquidity to pay off remaining debts, or to pay for their own funeral expenses, or to leave a tax-free legacy, should one or both spouses pass away. Again, they’re generally not using life insurance for job-related income replacement.

If you leave your employer and want to continue your life insurance, but don’t think you are healthy enough to quality for life insurance on your own, then the portability or conversion options can be a solution (see below). If you are in good health, you can shop for life insurance through your many local licensed agents.

PORTABILITY

Portability can be a good short-term solution, especially for workers who want to maintain life insurance coverage while they are between jobs. Under the portability option, you remain part of your past employer’s plan, but now you must pay the premiums since they’re no longer subsidized by your employer. You don’t have to prove your “medical insurability,” but since portability is supposed to be a short-term solution, your premiums will continue rising sharply each year that you maintain the policy.

THE CONVERSION OPTION

Conversion is a longer-term option than portability. It’s also more expensive. Conversion makes sense for people who don’t think they will be considered healthy enough to pass a standard physical exam or make it through the underwriting process, as this will not be required. Conversion allows you to purchase an individually owned Whole-Life policy (not your employer’s), from the same insurance company that offers the group life plan through your former employer. The Whole Life policy is designed to last no matter how long you live, with a guarantee that the premium will never increase. However, under this type of plan, your policy will be more expensive than it was as an employee. That’s due to what the insurance industry calls “adverse selection,” i.e. it’s riskier for the insurer to cover you because they don’t know how potentially poor your health may be.

REVIEW EMPLOYER STOCK AND NET UNREALIZED ASSETS (NUA) STOCK

CONCENTRATION STOCK RISK

Many of our clients hold large blocks of their employer’s stock. These holdings typically comprise shares they have accumulated over the years via their 401(k) plans, their stock options, or their discounted employee stock purchase plans. While holding large amounts of employer stock seems like the right thing to do as a loyal employee, it can be very risky. Do you really want to leave your family’s financial future vulnerable to the ups and down of a single stock or industry (i.e. your employer’s?). No matter how strong a company you work for (or worked for), there are a wide variety of factors that can rapidly decrease the value of your employer’s stocks. As a rule of thumb, I don’t recommend holding more than 10-percent of your net worth in any single stock—including company shares. No hard feelings, just diversify.

TAX CONSEQUENCES OF STOCK HELD OUTSIDE A 401(K)

In addition to the words of caution above, there are several other things to be aware of when you have employer stock owned outside of your retirement account. In a “taxable” non-retirement account, you will NOT simply pay ordinary income taxes on all of your distributions like you would in a traditional IRA or 401(k). You will have either a capital gain, or loss, for each “lot” of stock you purchased or were awarded. (If the stock pays an ordinary dividend, then that may also be taxed as ordinary income tax rates.)

You need to make sure that the cost basis for each lot you own is accurately recorded with the broker who holds them! If it isn’t, find your broker(s) ASAP before you decide to sell any of the stock. If you have held these stocks for a long time, chances are they have generated significant taxable losses (or gains) that will have big consequences for you.

If you recognize that you indeed have a large “unrealized” GAIN, you may want to think twice about selling the stock, or maybe even spreading out those sales, and related tax consequences, over several years.

If you recognize that you have a large unrealized LOSS, you may want think carefully about how ready you are ready to realize that loss now—or do you believe the company stock value will rise again? If you decide that you need the cash now or would like to diversify and sell the stock at a loss, you will “bank” that loss until it is offset by capital gains in the future. Under current law, those losses will not expire and you may retain this “loss carry forward” for a very long time. This is actually a nice consolation prize.

EXAMPLE: If you had a $200,000 capital loss realized, then you would have $200,000 of capital gains that you could realize any time in the future without owing any taxes!

UTILIZING NUA FOR STOCK INSIDE A 401(K)

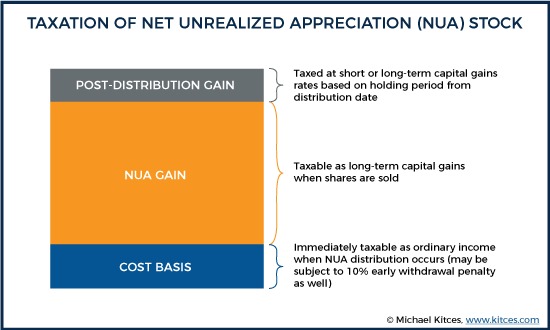

Not everyone has the ability, or desire, to own employer stock inside their 401(k) retirement plan. If you do, be aware of your options for that employer stock when you decide to move those stocks out of your 401(k) plan into an IRA. Most retirees will “rollover” their entire 401(k) into an IRA, which means all of the investments held inside the 401(k) are sold and deposited into the IRA as cash. A complex and little known strategy is to utilize your Net Unrealized Appreciation (NUA) in your employer stock inside your 401(k). The NUA is the gain you have achieved in the employer stock you own above your cost basis (i.e. what you paid for it). You can elect this special tax treatment by moving these shares into a non-retirement account.

The key benefit of this strategy is that you will pay long term capital gains tax on those future distributions. This is opposed to paying ordinary income tax rates on what you would have paid on those future distributions had they been from a traditional IRA. For certain people, the capital gains rate can be half the rate of their ordinary income tax. However, this is not always the best strategy to elect. Should you want to elect the NUA distributions, you will need to pay ordinary income taxes on the entire cost basis of those shares in the year you move them from your 401(k) into your taxable account. Therefore, the lower the cost basis and the larger the gain in your stock, the better this option will be for you. For many of my clients, this strategy it is not advantageous. But, for the few who have owned their stock for a very long time, and who have a large gain and low cost-basis, it will save them a tremendous amount of taxes.

Always remember to consult your CPA and Certified Financial Planner before executing the NUA strategy.

CONCLUSION

Workforce reductions are never easy, regardless of your age, industry or stage of career. But, by staying calm and getting your financial house in order as a job-seeker, consultant or retiree, you can substantially increase your odds of landing your next great career opportunity or getting a rewarding jump start on retirement.

About the author

Erik Dullenkopf, CFP® is the founder of Ventura-California-based Screaming Eagle Wealth Management. The firm specializes in working with families in the energy & agriculture industry and guides them in successfully managing their transition into and throughout retirement. By focusing on this niche, Erik and his team brings unique knowledge and insight about the commonalities, struggles and benefits that the ever-changing oil and gas industry faces.